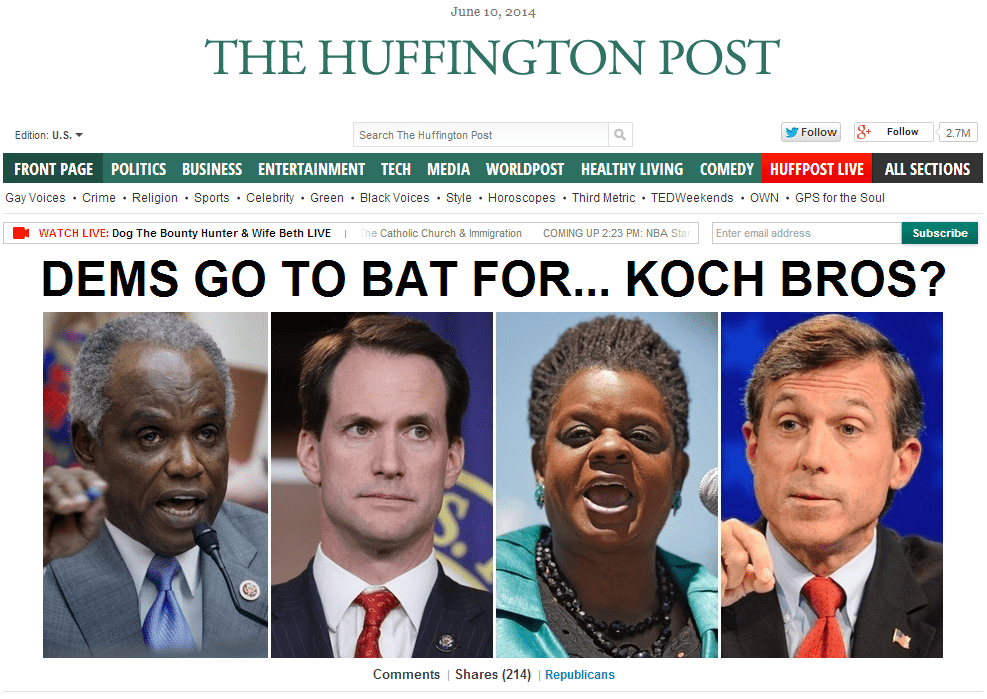

The House is currently working on a bill that would re-authorize the Commodity Futures Trading Commission, usually not a controversial event, but this year, those who are looking to unravel Dodd-Frank have wrapped into this bill a number of items that specifically work to give banks more freedom to bankrupt us again. John Carney is right in the middle of this effort to continue to destabilize Dodd-Frank, and in the process, give the Koch Brothers an assist. Here’s the earlier Huffington Post front page announcing how Democrats — even our Democrat — are working to help the Koch Brothers:

In a bitter irony for Democrats, two of the people who stand to gain the most from the fracas are none other than Charles and David Koch, the Republican billionaires who have tapped one of the world’s largest fortunes to cut down Democrats in elections and fuel conservative reforms. According to a lobbying disclosure form, lobbyists for the Koch empire have pushed for four of the most controversial deregulation provisions in Cantor’s latest endeavor.

The Koch and Wall Street-backed deregulation items have all been folded into a bill formally reauthorizing the existence of the Commodity Futures Trading Commission — the regulator that oversees the multi-trillion-dollar derivatives market. The agency has been functioning without authorization since October, and financial oversight advocates are confident that it can continue to do so unless the GOP passes legislation to defund it.

By lumping a host of bipartisan bills together, the CFTC bill is Wall Street’s best chance yet to defang Dodd-Frank. The most consequential deregulation bill in the package was introduced in early 2013 as HR 1256. Critics on Capitol Hill blast it as the “London Whale Loophole Act,” because it allows U.S. firms to skip Dodd-Frank’s trading rules on derivatives, provided they conduct trades in other countries with supposedly similar regulatory regimes.

The bill’s two Democratic co-sponsors Reps. David Scott (D-Ga.) and John Carney (D-Del.), denied meeting with Koch lobbyists, as did two Democrats who co-sponsored a previous version of the bill in 2011, Reps. Gwen Moore (D-Wis.) and Jim Himes (D-Conn.). Of the 17 Democrats on the House Financial Services Committee who voted for the bill in committee last spring, 10 denied meeting with the Kochs, and seven did not respond to requests to comment. Most insisted they had no idea the Kochs were pushing for the bill.

This election cycle, Moore has collected $243,400 from the financial industry, according to data from the Center for Responsive Politics — nearly triple the $89,750 she’s raised from organized labor, her next-highest backer. Scott has pulled in $220,160 from finance, compared with $68,000 from unions. The $353,632 Carney has drawn from the financial industry is more than five times what he’s received from his next-biggest supporter, lawyers and lobbyists. Himes, who has been in charge of national fundraising for House Democrats since early 2013, has secured $733,600 from the banking sector for his own war chest and political action committee (the Center for Responsive Politics categorizes his next-highest sector as simply “other”).

You should read the whole thing to get the entire context. But keep in mind that John Carney is doing more work to make sure that Too Big To Fail is permanent government policy than he is in making sure that your Social Security is secure and available to you. He will tell you that your Social Security benefits need to be reduced for the good of the system, yet making it easier for Banks to make their way to the trough is the (not very fiscally responsible) work he is committed to doing.