![]()

State Representative Bryon Short was on Facebook over the weekend highlighting this study that argues that Delaware has the best tax system in America, in that it is the least regressive (i.e. taxes the poor and lower and middle classes of income earners more than the top earners). I thought to myself, how the hell could that be? Someone early $60,000 pays the same tax rate as someone making $6 million under the state income tax scheme.

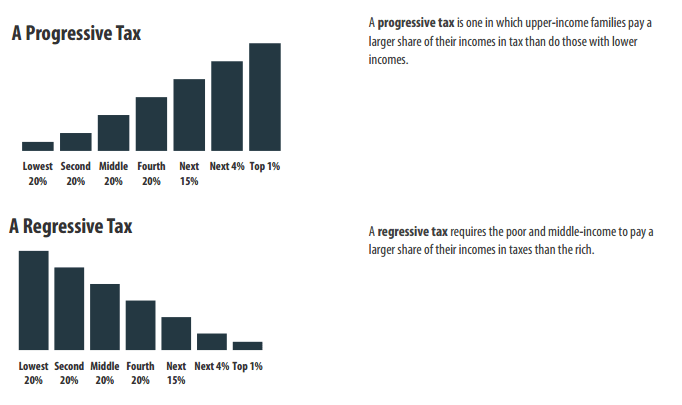

What I was forgetting is the “no sales tax.” Sales and other consumption taxes are very regressive because they fall most disproportionately on the poor. And that is the sole reason we are the least regressive tax system in America.

Delaware’s income tax is not very progressive, but its high reliance on income taxes and low use of consumption taxes nevertheless results in a tax system that is only slightly regressive overall.

Let’s define our terms here. A progressive tax is not necessarily a tax that the PDD or Delaware Liberal would like (although it is). This chart explains:

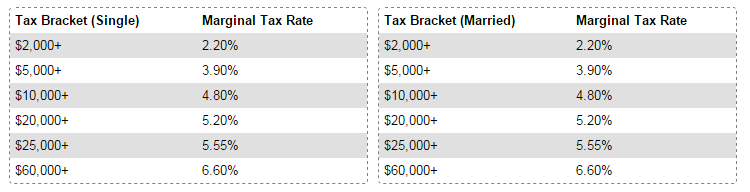

Delaware has a very regressive income tax structure, as described above and shown below:

For incomes above $60,000, Delaware essentially has a flat tax. So that is why when I first saw this headline being touted by a Democrat, of all people, I did a double take. Mr. Short, you need to stop. Delaware is not the least regressive state on income taxes. It is one of the most regressive state. So you, Mr. Short, need to use your power as a Committee chair to make Delaware’s income tax more progressive.

How do we do that? Let’s start by making the Earned Income Tax Credit fully refundable.

Perhaps the most important factor enhancing income tax fairness in recent years has been the proliferation of low-income tax credits. These credits are most effective when they are refundable — that is, they allow a taxpayer to have a negative income tax liability which offsets sales and property taxes — and are adjusted for inflation so they do not erode over time.

Twenty-five states and the District of Columbia have enacted state Earned Income Tax Credits based on

the federal EITC. Calculating a state EITC as a percentage of the federal credit makes the credit easy for state taxpayers to claim (since they have already calculated the amount of their federal credit) and easy for state tax administrators to monitor.Refundability is a vital component of state EITCs to ensure deserving families get the full benefit of the credit. Refundable credits do not depend on the amount of income taxes paid: if the credit exceeds income tax liability, the taxpayer receives the excess as a refund. Thus, refundable credits usefully offset regressive sales and property taxes and can provide a much needed income boost to help families pay for basic necessities. In all but four states (Delaware, Maine, Ohio and Virginia), the EITC is fully refundable.

That is an embarrassment for Delaware, and it must end now. Make the EITC fully refundable. Now.